“It’s highly probable that a great many investors will look back on 2020 and wonder how they missed these signs of a new commodity bull market.”

Prices have surged to highest in more than six years

Inflation fears are drawing investors back to resources sector

For the best part of a decade, commodities have been deeply out of fashion. Now, as investors scour the market for the great reflation play, they’re hot again.

Investing luminaries from Point72 to Pimco are calling for commodity prices to move higher. Goldman Sachs Group Inc., the bellwether of Wall Street, is predicting a new commodity bull market to rival the China-driven boom of the 2000s and the oil price spikes of the 1970s.

“We very much believe that the fundamentals are now in place for a new, structural, bull market to begin,” said Robert Howell, senior research strategist at Gresham Investment Management LLC, the commodities-focused unit of Nuveen with $5.8 billion in assets in the sector. “In the years to come, it’s highly probable that a great many investors will look back on 2020 and wonder how they missed these signs of a new commodity bull market.”

Joseph Safra became the world's richest banker by transforming a Brazilian lender into a global multibillion-dollar empire.

Now, after a long illness and death at 82, it falls to the next Safra generation.

What's at stake is a conglomerate which comprises Banco Safra SA, Safra National Bank of New York and Switzerland's J Safra Sarasin -- firms with about $85 billion in banking assets. There's also a $2.3 billion real estate portfolio, that includes the Gherkin in London and 660 Madison Avenue in New York, a stake in banana company Chiquita Brands International and a 130-room mansion in Sao Paulo.

Together, his four children and widow stand to inherit a fortune estimated at around $17.6 billion, according to the Bloomberg Billionaires Index.

...

"Safra's importance in the financial system is smaller today then it once was. Other banks outgrew it," said Rafael Schiozer, a professor of Finance at Fundacao Getulio Vargas. "The family now faces challenges both in defining a strategy for its businesses and who will control them.

Safra "leaves a legacy that will be followed by many generations," according to a statement from Banco Safra on Thursday that said he died of natural causes. The bank didn't respond to a message seeking further comment.

The Safra dynasty traces its origins to the Ottoman Empire, when it financed camel-caravan traders, and has endured global and family crises.

Joseph Safra was born in 1938, in Beirut, Lebanon, to a Jewish banking clan with roots in Aleppo, Syria. His father, Jacob, moved the family to Brazil after World War II and Banco Safra was established in 1957. He and his brother Moise ran the Brazilian business, after their elder brother, Edmond, had broken off years before to build his own banks in Europe and New York.

Edmond, who later sold the business to HSBC Holdings Plc, died in 1999 as a victim of arson in Monaco.

In Brazil, Joseph and Moise grew the bank into one of Latin America's biggest, catering to the country's wealthiest people and most prominent companies. The business was known for its soundness, withstanding the many turbulences its home nation threw at it.

Jack Manning/The New York Times/Redux

Jacob Safra famously said: "If you choose to sail upon the seas of banking, build your bank as you would your boat, with the strength to sail safely through any storm."

It also had misteps, including in 2009 after the group was linked to a feeder fund for Bernie Madoff, who orchestrated a $17.5 billion Ponzi scheme.

Joseph and Moise split in the 2000s, when a falling out between the two led Joseph to create a rival lender across the street from his family's, J Safra, and started poaching clients. To end the dispute, Moise sold his share of the family business to Joseph in 2006 for a reported $2.5 billion and left the bank.

Joseph Safra, who had parkinson's disease, did make arrangements for his succession. His children Jacob, David, Alberto and Esther were all granted shares of the family's main asset, Banco Safra, last December, according to a regulatory filing. Two of his sons already have central roles within the group, with Jacob running the international side of the operations, while David oversees the Brazilian firm.

Joseph's middle son, Alberto, departed from the board of his family lender in 2019, due "exclusively to his personal intent of dedicating himself to another project with the family," according to a memo sent by Safra at the time. Alberto kept his stake at Grupo J. Safra and created ASA Investments. Joseph's daughter, Esther, is an educator and was never involved with the bank.

"Joseph, Moise and Edmond had their differences at their time, disagreeing on how to handle the business, and the next generation might have their disagreements too," said Rodrigo Marcatti, a former Safra employee who's now chief executive of Veedha Investimentos.

The younger Safras are already making their mark. The Brazilian unit, built to serve the wealthy and the nation's biggest firms, ventured into retail banking this year. In October it launched AgZero, a digital bank with no branches, while beefing up a digital investment platform under the SafraInvest brand. Notoriously low-profile, the lender has invested more on marketing.

There are also subtler changes. Last year, David was seated arm-in-arm with the rest of the nation's banking elite at a year-end luncheon hosted by the Brazilian federation of banks. At those sorts of events, Banco Safra was usually represented by a high-ranking executive, not a family member -- Joseph was incredibly media shy, rarely gave interviews and avoided public events. David's presence was seen as a show of force within the firm.

"Safra was always a traditional bank, but being traditional doesn't mean it's not evolving," Schiozer said. "What differentiates it is that Safra is seen as safe, no one is afraid of doing businesses with it.

In all, suspicious activity reports in the FinCEN Files flagged more than $2 trillion in transactions between 1999 and 2017. Western banks could have blocked almost any of them, but in most cases they kept the money moving and kept collecting their fees.

Read the whole investigation on BuzzFeed News here:

Deadly Terror Networks And Drug Cartels Use Huge Banks To Finance Their Crimes. These Secret Documents Show How The Banks Profit.

BNP Paribas SA is shutting its Swiss commodity trade finance business, exiting a sector it once dominated but has been hit by a series of massive frauds.

The former Paribas investment bank's office in Geneva helped pioneer the use of letters of credit to finance oil trading in the 1970s, and became one of the leading lenders to the industry. However, BNP Paribas had been shrinking in commodity trade finance since 2014, when it was fined $8.9 billion for violating U.S. sanctions.

The plan could impact as many as 120 employees in its Geneva offices, the French bank said in a statement late Tuesday.

Weber und Rohner prüfen angeblich UBS-CS-Fusion | Unternehmen Finanz | Finanz und Wirtschaft

Sounds like bad news for Switzerland's banking sector to have such a high concentration of power in one institution...

Weber und Rohner prüfen angeblich UBS-CS-Fusion

According to a media report, the board presidents of the two big banks are sounding out a possible merger.

(AWP) The two major Swiss banks UBS ( UBSG 11.3 1.3% ) and Credit Suisse ( CSGN 10.02 1.89% ) want to merge according to a media report. UBS Board of Directors President Axel Weber is planning a merger with CS President Urs Rohner, writes the finance portal "Inside Paradeplatz" on Monday.

The project is called Signal, according to the report from inside the two big banks. Weber was the driving force behind it and spoke to Finance Minister Ueli Maurer about it, said an informant according to the portal. The financial market regulator Finma is also in the picture about Weber's plans. The merger should be agreed in early 2021, and at the end of 2021 Switzerland would have a new financial giant.

It now seems the mother of all short squeezes may finally be near, as more and more investors take Physical Delivery of Gold, rather than roll over their Futures Contracts...

"Just like a fear of cash shortages would cause a run on the banking system, fears of physical precious metals shortages could cause a run on whatever is left in the COMEX warehouses."

"While the COMEX claims there is enough gold in registered to satisfy current deliveries, we have started to see some anomalies in the data which potentially paint a different picture."

Interesting piece on how the fudging of the numbers on the COMEX is going to come around and bite them in the …, sooner rather than later, as more and more people are taking delivery of physical metal vs. rolling over their paper contracts... this has been going on for years, but the potential short squeeze is becoming more glaring as the pumping of liquidity, without any real backing, goes into overdrive.

"while the COMEX allows as many paper derivative contracts to be placed as bets on the market price,we only have a finite amount of the real metals available on the market at any given time. Those cannot be printed up at the push of a button on a computer like the paper contracts can be.This has two effects on the market.

"First, when the physical deliveries are miscounted, the paper contract derivative trades overstate short term speculative interest in the metals versus those willing to take ownership. Secondly, and probably more importantly, it overstates the amount of physical metals available for delivery on the futures market for those that want to take delivery. It basically amounts to fraud, much as if your bank claimed to have enough cash for your deposit, and then notified you when you showed up to the bank that you would have to wait 2-3 months to get your cash."!!!

Clear Outperformance of #Gold since 2000 vs. $SPX, Bonds & $USD

Gold Needs to "Glow Up"

As of August 24, gold bullion1 has gained 27.13% YTD and 39.74% YOY. Gold mining equities (SGDM)2 are up 38.85% YTD and 61.54% YOY. This compares to 7.55% YTD and 11.96% YOY returns for the S&P 500 TR Index.3 Silver has posted outsized gains, climbing 49.03% YTD and 50.00% YOY.

Gold is a Mandatory Portfolio Asset

Now that gold has powered over $2,000, it's an excellent time to take stock of what has been accomplished by the monetary metal and what may lie next. As for my Gen-Z "Glow Up" reference (and more below), conversations with my 16-year-old daughter are a constant reminder that I, too, like the gold market, need some updating and modernization.

Most importantly, in our view, it has been established as a baseline that a diversified asset portfolio must include an allocation to gold. We believe this statement is justified by the fact that gold is now the only monetary asset that is priced by a liquid-free market and not directly correlated and partially controlled by central bank (i.e., government) policies and market interventions.

Without once again judging the merits of the exceptional monetary debauchery and fiscal stimuli of 2020, and regardless of an investor's views on credit and equity market valuations or prospects for inflation, there is no other liquid asset which accomplishes what gold does in the way of portfolio insurance and purchasing power protection.

"Software projects with our nation's defense and intelligence agencies, whose missions are to keep us safe, have become controversial, while companies built on advertising dollars are commonplace. For many consumer internet companies, our thoughts and inclinations, behaviors and browsing habits, are the product for sale. The slogans and marketing of many of the Valley's largest technology firms attempt to obscure this simple fact."

The full letter is below:

Palantir CEO rips Silicon Valley in letter to investors

With McKinsey's help, Wirecard hatched a plan to acquire Deutsche Bank, offering the German FinTech the prospect of a miraculous exit from the massive fraud it had been perpetrating.

By blending Wirecard's business into Deutsche's vast balance sheet, it hoped it could be possible to "somehow hide the missing cash and explain it away later in post-merger impairment charges."

There was one catch. To even start preparing such a deal in earnest, the company needed to get a clean bill of health from KPMG, which was conducting a special audit of Wirecard's books.

Six months later the curtain fell on Wirecard. On June 25, the group collapsed into insolvency after it was exposed as one of Germany's biggest postwar accounting frauds. Prosecutors in Munich suspect that €3.2bn in debt raised since 2015 has been "lost". Around €1bn was handed out in unsecured loans to opaque business partners in Asia.

Wirecard: the frantic final months of a fraudulent operation

Executives at the German payments group hatched a plan to buy Deutsche Bank while desperately trying to cover their tracks

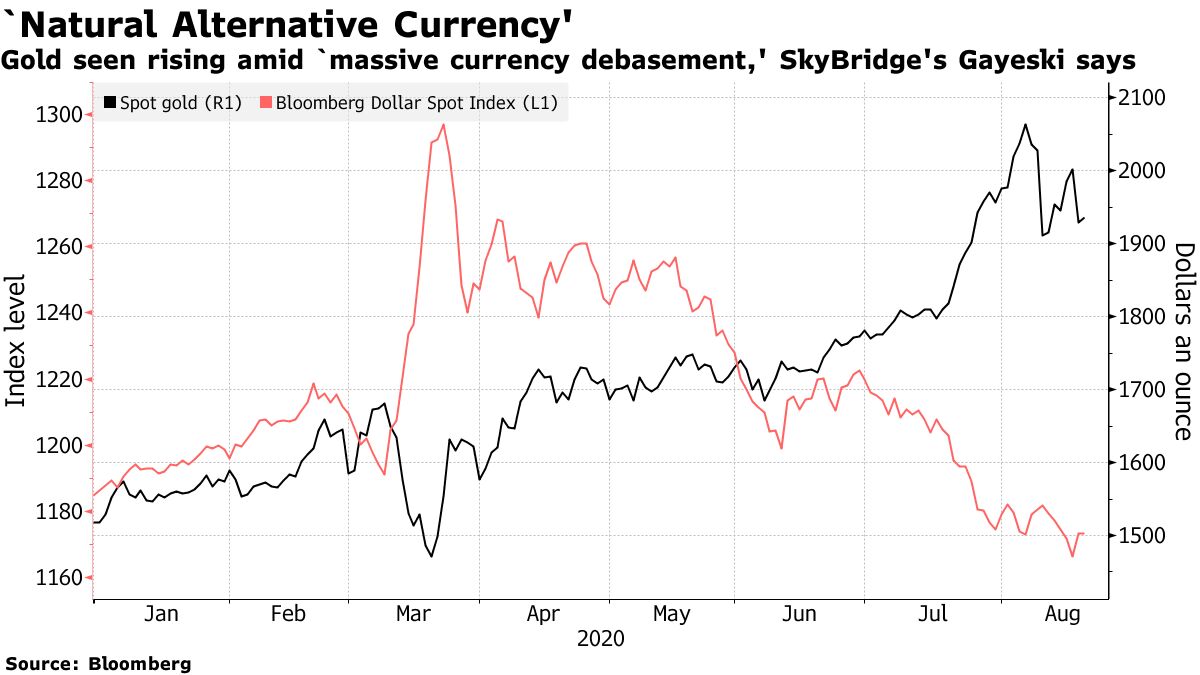

Gold to Gain on Massive Currency Debasement, SkyBridge Says - Bloomberg

Gold to Gain on Massive Currency Debasement, SkyBridge Says

Gold will extend its record-setting rally on "massive currency debasement" and expectations for further stimulus, according to SkyBridge Capital, which recently added exposure to the metal after exiting in 2011.

"When you think of currency debasement the question is, what is the dollar going to weaken against, and when you look around the globe, it's hard to be excited about alternative currencies," said Troy Gayeski, co-chief investment officer and senior portfolio manager, listing the euro, yuan and emerging-market monies. "So, gold is obviously a natural alternative currency."

The precious metal surged to a record well above $2,000 an ounce earlier this month -- although prices have stumbled since then -- as central banks including the Federal Reserve unleashed vast stimulus to support economies hurt by the coronavirus pandemic. That's spurred bets that paper currencies will lose their value as money supply jumps. Goldman Sachs Group Inc. calls gold the currency of last resort and has forecast more gains.

Gold is "fairly rich versus oil or other real commodities, but it hasn't appreciated nearly as much as money-supply growth since its previous peak in September of 2011," Gayeski said in an interview. "It wouldn't surprise us if by the end of next year, it's around the $2,100-to-$2,200 range."

Spot gold hit an all-time high of $2,075.47 an ounce on Aug. 7 as the dollar weakened and real interest rates fell well below zero. On Thursday it climbed 0.4% to $1,936, up almost 28% this year. Prices eased midweek after minutes from the Fed showed it edging away from a step that would underscore a commitment to an extended period of ultra-loose policy.

Ultimately, the driver for gold is "you have massive currency debasement, particularly in the U.S.," Gayeski said.

SkyBridge, which manages $7.35 billion, has about 3% exposure to gold, with the majority of positions taken in the past two months. The fund-of-funds manager's primary exposures are to U.S. cash-flow-generative strategies backed by tangible assets, including residential mortgage-backed securities.

While the latest round of fiscal stimulus talks haven't yet yielded a deal, the Fed has already swelled its balance sheet by about $2.8 trillion this year, with Goldman cautioning that U.S. policy is triggering debasement fears.

The Fed will likely ramp up asset purchases, and there's more fiscal stimulus coming too, according to Gayeski. "All those things argue for a continued bull market in gold, again driven principally by money-supply growth and dollar debasement as opposed to real inflation fears," he said. "Furthermore, expect continued asset inflation long before real inflation ever shows up."

After rising 17 per cent in the first half of the year, gold prices surged to record highs before retreating on Tuesday to just below $2,000. In the process, investors went from treating gold as a short-term momentum trade to seeing it more as a legitimate standalone option in long-term portfolios. You need only look at real yields on government bonds after adjusting for inflation to see why so many investors are buying gold as a long-term option.

Gold's evolution into a 'must-have' asset is storing up trouble

Price rise is being driven by investors adding the metal to long-term portfolios

The writer is Allianz's chief economic adviser and president-elect of Queens' College, University of Cambridge

Until recently, the rapid rise in the price of gold had more to do with opportunistic financial trading than any larger structural investment theme, let alone a drop in physical supply or an increase in industrial use.

Now, the metal is seen to offer something for everyone. That is yet another unintended result in a lengthening list of the exceptional involvement of central banks in the functioning of markets. Their expanded interventions to counteract the effects of the pandemic have pleased many now but will create problems for the central banks and the economy at large, if a sharp and lasting economic recovery continues to elude us.

After rising 17 per cent in the first half of the year, gold prices surged to record highs before retreating on Tuesday to just below $2,000. In the process, investors went from treating gold as a short-term momentum trade to seeing it more as a legitimate standalone option in long-term portfolios. You need only look at real yields on government bonds after adjusting for inflation to see why so many investors are buying gold as a long-term option.

Contrary to what most textbooks would suggest, the recent drop in nominal yields has coincided with a rise in inflationary expectations. This makes gold a more attractive substitute for government bonds in two ways. Investors who opt for gold forgo less income than they would if bond yields were higher. They also hedge against what would be a dramatic loss in the value of those bonds, should central banks stop trying to keep interest rates low by flooring official rates and buying massive amounts of market securities.

Gold is also proving compelling for other reasons, collecting quite an unlikely cast of backers in addition to the usual bugs who worry about currency debasement and geopolitical shocks. Some believe it will protect investors against further depreciation of the US dollar; others want it as a hedge against a global economic depression and a collapse in stock markets that, already, are stunningly decoupled from corporate and economic realities. Today's gold camp even manages to attract those looking to protect against competing outcomes: deflation and inflation.

Gold is not the only asset to have developed this multiple and seemingly bipolar personality. Big Tech stocks have also been seen as offering everything to everybody. They promise growth based on the shift from physical to virtual activities in the pandemic, but also downside protection because they have massive cash holdings, low debt and positive cash-flow generation. The collapse in nominal yields on government and safe corporate bonds is also leading some investors to ask whether non-investment grade "junk" bonds can be a safe place to park their money.

Underpinning these contradictory developments is investor faith that central banks will protect them from big losses by continuing to intervene whenever markets slide. Gold is evolving into a "must-have" asset. That drives the price upwards as the pool of potential buyers shifts from a small group of quirky bugs to the much larger pool of investors seeking risk mitigation. Like many sudden structural shifts, it is likely to involve an initial price overshoot.

Think of this as part of a broader shifting baseline. Investors are treating an ever growing number of traditionally risky assets as low risk, or even hedges against risk. In the short term, this pushes prices higher, reinforcing the attitude change and lulling politicians and central bankers into believing that the market cycle has been conquered. But they are likely to prove as wrong as those who, before the 2008 financial crisis, erroneously believed they had vanquished the business cycle.

The map above is one of my all time favourites. It shows Pangaea, a supercontinent that existed from 300 million to 175 million years ago, with modern international borders.

Needless to say it would make international relations a little bit more complicated. Major changes include:

The United States now borders a few new countries including Morocco, Mauritania, Senegal and Cuba.

Spain now has a land border with Algeria.

Italy now borders Tunisia.

Greece borders Libya.

Brazil borders a whole bunch of new states from Namibia in the south to Liberia in the north.

India now finds itself in the southern hemisphere, right next to Antarctica.

You could walk from Australia to Tibet (which is no longer attached to China).

While China has lost Tibet it has gained a massive amount of new coast line.

Notice anything else that might complicate international politics? Then please, leave a comment in the comment section below.

"when regular money rates become negative, however, gold's zero yielding quality is no longer construed as a vice but rather a feature. In such circumstances, holding cash becomes costly while holding gold becomes the opportunity. And it's this feature which triggers not just demand for new sources of gold, but also a backwardation that incentivises those who have previously stashed gold to sell out at a profit."

Read the whole piece here: http://ftalphaville.ft.com/2020/08/05/1596631139000/What-s-with-gold-backwardation-/

Why private capital will benefit from the crisis | Financial Times

"Given the exuberant growth, many observers had predicted the private capital industry would be hit hard in a downturn."

"But perhaps this is merely the end of the beginning of a new era of private capital, rather than the beginning of the end."

…

"Before, investors could kid themselves that they could wait until bond yields approached normality, but normality has now been redefined. Most investors still hanker after returns in the 7-9 per cent range. Private markets are pretty much the only areas where this looks feasible.

"At the same time, companies are tiring of the burdens and relentless daily scrutiny that goes with being publicly listed. The trend towards businesses remaining private is likely to be accentuated by the crisis. While more companies have been raising money in the bond market, it remains a viable option for big businesses only. Smaller ones are likely to turn to private debt funds in even greater numbers to cope with the downturn."

US Bank Stocks Sink As Fed Caps Dividends, Forbids Share Buybacks In Stress Tests | Zero Hedge

Fed said in a release that big banks will be required to suspend share buybacks and cap dividend payments at their current level for the third quarter of this year.

The Board is taking action to assess banks' conditions more intensively and to require the largest banks to adopt prudent measures to preserve capital in the coming months."

Bank stocks are not happy...

Wells Fargo and BofA are the worst hit after hours...

Ally Financial and BMO had the lowest common equity tier 1 ratio in the severely adverse scenario:

Discover, Capital One, Barclays, and Amex face the biggest loan losses...

Credit Suisse is the most exposed to losses from Commercial Real Estate...

* * *

So what did the results say?

The Fed said in a release that big banks will be required to suspend share buybacks and cap dividend payments at their current level for the third quarter of this year. The regulator also said that it would only allow dividends to be paid based on a formula tied to a bank's recent earnings.

Furthermore, the industry will be subject to ongoing scrutiny: For the first time in the decade-long history of the stress test, banks will have to resubmit their payout plans again later this year.

"While I expect banks will continue to manage their capital actions and liquidity risk prudently, and in support of the real economy, there is material uncertainty about the trajectory for the economic recovery," Fed Vice Chair Randall Quarles said in a statement.

The Federal Reserve Board on Thursday released the results of its stress tests for 2020 and additional sensitivity analyses that the Board conducted in light of the coronavirus event.

"The banking system has been a source of strength during this crisis," Vice Chair Randal K. Quarles said, "and the results of our sensitivity analyses show that our banks can remain strong in the face of even the harshest shocks."

In addition to its normal stress test, the Board conducted a sensitivity analysis to assess the resiliency of large banks under three hypothetical recessions, or downside scenarios, which could result from the coronavirus event. The scenarios included a V-shaped recession and recovery; a slower, U-shaped recession and recovery; and a W-shaped, double-dip recession.