Charlie Munger is Warren Buffett's partner in crime and Co Chairman at Berkshire Hathaway.

"I never allow myself to have an opinion on anything that I don't know the other side's argument better than they do." — Charlie Munger

***

While we all hold an opinion on almost everything, how many of us do the work required to have an opinion?

The work is the hard part, that's why people avoid it. You have to do the reading. You have to talk to anyone competent you can find and listen to their arguments. You have to think about the key variables and how they interact. You have to listen and chase down arguments that run counter to your views. You have to think about how you might be fooling yourself. You have to see the issue through multiple lenses. You need to become your most intelligent critic and have the intellectual honesty to kill some of your best-loved ideas.

"We all are learning, modifying, or destroying ideas all the time. Rapid destruction of your ideas when the time is right is one of the most valuable qualities you can acquire. You must force yourself to consider arguments on the other side." — Charlie Munger

As Rabbi Moses ben Maimon (1135–1204), commonly known as Maimonides, said:

"Teach thy tongue to say I do not know, and thou shalt progress."

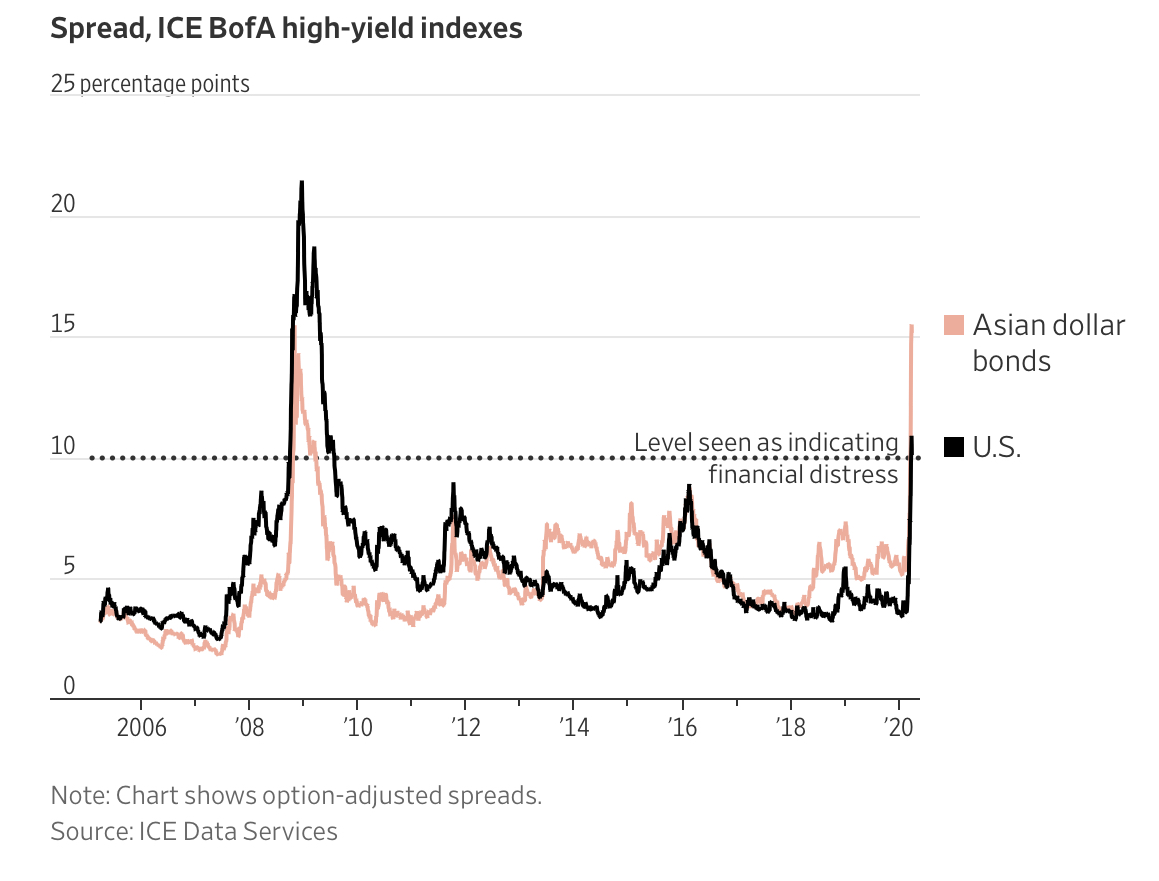

More than 1,400 bonds—43% of those tracked in an influential $2.1 trillion index of global junk bonds—are currently trading at what investors consider distressed levels, with yields that are more than 10 percentage points above those on risk-free U.S. Treasurys, vs. less than 450 three weeks ago, before the rout began.

Emergency: SMEs Face A Global Crunch Drowned In Liquidity

We will see, again, the bailout of the reckless and the burden to the prudent.

From Hedgeye:

Emergency: Small Businesses Face A Global Crunch Drowned In Liquidity

The guest commentary below was written by Daniel Lacalle.

Many countries have decided to lock down entire cities and shutdown airspace to contain the spread of coronavirus. This decision may create a massive crisis drowned in liquidity.

Governments and central banks are committed to do whatever it takes in terms of demand-side policies, spending and increasing liquidity as much as needed to avoid a 2008-style crisis. However, these measures, which were already ineffective for years, will be even less successful this time.

To start with, global policymakers made the mistake of implementing aggressive easing policies in a period of growth, which left them without effective tools to address the financial turmoil. When central banks cut rates and inject billions of liquidity in a period of growth and risk appetite, an urgent reaction due to a black swan scenario like coronavirus finds them with no tool that makes a significant impact.

What impact will the ECB have with a 120 billion euro per month asset purchase when it has already bought almost 20% of eurozone governments' debt in its misguided monthly 20 billion euro purchase and deposit rates are negative? None. Sovereign debt in the eurozone already trades with a negative yield, and buying corporate bonds of zombie multinationals did not help the eurozone economy nor will it help now.

Adding a monetary facility for SMEs only helps those who are indebted now, it does nothing for those small and medium companies that were prudent all throughout these years and now face a collapse in sales and accumulating fixed costs.

The Spanish government launched an urgent economic program of tax relief that, when you read the text, only applies to companies with sales below 6 million euros and maximum relief of 30,000 euro. Nothing. The vast majority of self-employed workers and small companies that face a lockdown that can last for months are not going to receive the slightest respite. In Italy, only the already indebted will see some relief. This is exactly the same all over Europe. Governments are implementing aggressive demand measures when the problem is not a demand issue and ignoring the real risks.

For most small companies and self-employed workers globally, a month of closure is a ruin. Two months is a catastrophe that leads to a domino of bankruptcies and layoffs.

The key factor is that the lockdown and economic crisis ahead comes on top of a very weak 2019 and 2018 for small companies, which are almost 90% of the corporate fabric in most developed nations.

Working capital kills more companies than the Government, but when the two factors come together, the risks of falling into a severe crisis are enormous.

What is death by working capital? Revenues plummet, rising unpaid or delayed payment invoices, while at the same time fixed costs accumulate and taxes continue to drown businesses. Most companies have very little liquidity. According to Moody's the large quoted companies have increased cash, but even at large multinationals -excluding tech giants and a few exceptions-, net cash balance sheet does not cover one year of working capital requirements, particularly in the eurozone. However, an average small company usually has enough cash to survive a maximum of two months of difficulties. Hardly enough to survive a complete shutdown and a pandemic crisis.

In 2019 there were already worrying signals. In the US, small businesses were struggling despite economic growth and low unemployment. Thousands of stores closed in 2019, and the statistics of Business Formation suggested a significant weakness ahead.

The mightiest Hedge Fund of them all, Renaissance Technologies, has been tripped up by the market turmoil unleashed by the coronavirus outbreak, underscoring how even the industry's brightest names are struggling to navigate the financial chaos.

If you want to Understand the Bitcoin Stock To Flow Model explained by PlanB himself, listen to Pomp's latest Off the Chain Podcast: Why Bitcoin's Stock-To-Flow Model Is Becoming More Accurate Over Time.

The Fed's half a percentage point rate cut may very well have been its best efforts at helping the struggling corporates. With sales dropping at least this rate cut will help with their cash flow when servicing their growing debts...

From the Financial Times:

The Seeds of the Next Financial Crisis

In the short term the behaviour of credit markets will be critical. Despite the decline in bond yields and borrowing costs since the markets took fright, financial conditions have tightened for weaker corporate borrowers. Their access to bond markets has become more difficult. After Tuesday's 50 basis-point cut, the US Federal Reserve's policy rate of 1.0-1.5 per cent is still higher than the 0.8 per cent yield on the policy-sensitive two-year Treasury note. This inversion of the yield curve could intensify the squeeze, says Charles Dumas, chief economist of TS Lombard, if US banks now tighten credit while lending has become less profitable.

This is particularly important because much of the debt build-up since the global financial crisis of 2007-08 has been in the non-bank corporate sector where the current disruption to supply chains and reduced global growth imply lower earnings and greater difficulty in servicing debt. In effect, the coronavirus raises the extraordinary prospect of a credit crunch in a world of ultra-low and negative interest rates.

...

A comparison of today's circumstances with the period before the financial crisis is instructive. As well as a big post-crisis increase in government debt, an important difference now is that the debt focus in the private sector is not on property and mortgage lending, but on loans to the corporate sector. A recent OECD report says that at the end of December 2019 the global outstanding stock of non-financial corporate bonds reached an all-time high of $13.5tn, double the level in real terms against December 2008.

The rise is most striking in the US, where the Fed estimates that corporate debt has risen from $3.3tn before the financial crisis to $6.5tn last year. Given that Google parent Alphabet, Apple, Facebook and Microsoft alone held net cash at the end of last year of $328bn, this suggests that much of the debt is concentrated in old economy sectors where many companies are less cash generative than Big Tech. Debt servicing is thus more burdensome.

...

In a downturn, some of the disproportionately large recent issuance of BBB bonds — the lowest investment grade category — could end up being downgraded. That would lead to big increases in borrowing costs because many investors are constrained by regulation or self-imposed restrictions from investing in non-investment grade bonds.

The deterioration in bond quality is particularly striking in the $1.3tn global market for leveraged loans, which are loans arranged by syndicates of banks to companies that are heavily indebted or have weak credit ratings. Such loans are called leveraged because the ratio of the borrower's debt to assets or earnings is well above industry norms. New issuance in this sector hit a record $788bn in 2017, higher than the peak of $762bn before the crisis. The US accounted for $564bn of that total.